SR Inc’s Virtual 2nd Quarter Symposium Includes Discussion on the Importance of Strong ESG Management in Responding to Rapidly Emerging Issues like the Coronavirus and Racial Unrest

SR Inc held its second quarter Sustainable Business & Enterprise Roundtable (SBER) Executive Symposium, originally scheduled to be in San Francisco, over Cisco WebEx on June 18th. Attendees heard from three leading executives at SR Inc Member-Client companies: Mike Mattera, Director of Corporate Sustainability at Akamai Technologies, Sean Kinghorn, Global Sustainability Leader at Intuit, and Andy Smith, Senior Manager of Global Energy Management & Sustainability at Cisco Systems.

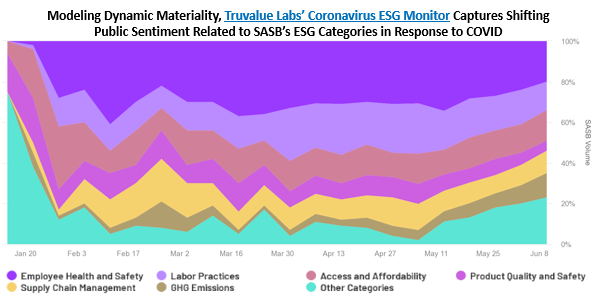

A key theme throughout the first half of the Symposium was the concept of dynamic materiality. Dynamic materiality recognizes that emerging issues can quickly shape how key stakeholders – like customers, employees, and host communities – make decisions about a company. When these issues emerge, they can quickly become material to a company’s financial investors. Therefore, current SEC regulations and related case law would suggest it is necessary for publicly traded companies to track and report efforts to manage these issues. The Covid-19 crisis may represent the ultimate example of dynamic materiality since managing the related risks has become an urgent priority for most customers, employees, suppliers, host communities, and, therefore, companies.

Writing for Forbes, Harvard Business School professor Bob Eccles (currently a visiting scholar at the Said Business School in London) highlighted the crisis of plastic pollution in the oceans as an example of an issue that quickly came to affect decisions of certain consumers. In a follow-up article, Eccles writes that the Covid-19 crisis represents a more dramatic example of dynamic materiality. Dynamic materiality is critically important because what environmental, social & governance (ESG) issues a company determines are material to its success become the focus of ESG management and reporting efforts. Over the last several years, ESG has skyrocketed to a CEO-level concern regularly managed by an ESG or Corporate Sustainability Committee that directs, tracks, and reports the company’s efforts on material ESG issues to investors.

As 2020 began, the interest in ESG-conscious funds grew from a rush to a stampede as over $30 trillion in global assets under management became subject to some kind of ESG screen. Five years earlier, Harvard Business School professor George Serafeim and colleagues published Corporate Sustainability: First Evidence on Materiality, which reflected their rigorous analysis on whether high performance on industry-specific ESG items [identified by the Sustainability Accounting Standards Boards (SASB)] were, in fact, financially material to investors. Serafeim concluded that the share value of companies with strong ESG programs outperform peer companies when normalized for size, age, and other factors. This helped turn conventional wisdom on its head and established that ESG-conscious investing was not only not concessionary but could also be an effective strategy for higher alpha returns.

By January of this year, Larry Fink of BlackRock (the CEO of the world’s largest investor) again underscored the importance of ESG in his annual letter to the 2,700 companies in which BlackRock invests. Fink told companies that they must track and report their management efforts regarding SASB-identified, industry specific ESG issues in a manner aligned with the Taskforce on Climate-Related Financial Disclosures (TCFD) and warns that non-compliance would lead to the possibility of shareholder action from BlackRock. Going even further, Fink shared that in response to overwhelming evidence that ESG high-performance is correlated with higher shareholder returns, BlackRock would increasingly use ESG-related analysis as part of its fundamental approach to investing.

As Fink was making this request, a highly infectious novel coronavirus had spread to human hosts throughout the sprawling urban communities of Wuhan and China. The Coronavirus was also being transported around the world by traveling, infected citizens of Wuhan – many of whom may have been asymptomatic. In the weeks that followed, news of this quick spreading virus impacted global financial markets and was initially perceived as a risk for companies with Chinese-dependent supply chains. But by the giant sell offs in early March, investors had come to recognize Covid-19 as a challenge to business operations everywhere.

In this environment, the ESG investment thesis – namely that companies that outperform peers in managing ESG risks and opportunities will outperform peers in shareholder performance – began to prove itself. In the painful global sell-offs in March, ESG high performing companies outperformed peers in share value. The well noted “flight to quality” in bear markets overlapped with investors staying invested in ESG high performers; as a Bank of America report found in March, “ESG is a bear market necessity, not a bull market luxury.”

Although global authorities influential in the field of corporate sustainability such as the World Economic Forum (described later in the blog) had long recognized the threat infectious diseases pose to global supply chains, the outperformance of ESG high performing companies in share value did not appear attributable to their superior managing of Covid-19 risks. Rather, the strong correlation between ESG high performers and strong share value performance during Covid-19 seems to be attributable to the fact that investors favor high quality (and ESG high performing) companies in uncertain markets.

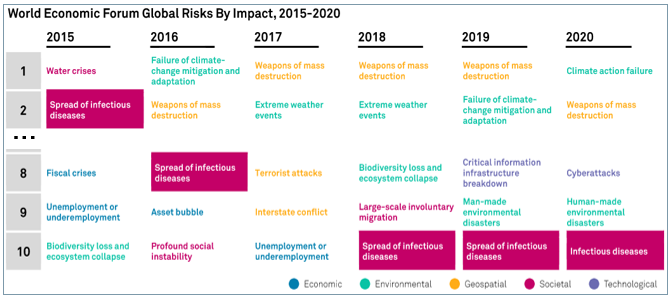

As we move out of the first six months of the Covid-19 crisis, it is likely that many companies will look to systemize how they address the risks and opportunities created by this crisis. Companies will likely want to move responsibilities to address Covid-19 and new pandemic-related risks beyond any emergency Covid-19 task forces. When this happens, many companies will likely recognize that the ESG or Corporate Sustainability Committee is the right “organizational home” to manage infectious disease-related risks. This is because Covid-19 is the ultimate ESG issue, as illustrated by these five reasons:

Conclusion

Corporate commitments to systemized and reported management of ESG issues was growing dramatically at the outset of 2020. The last few months have brought extra-financial exogenous issues like the Coronavirus and the needed and swelling demands for racial equity to the fore as well. As companies effect the acute changes required by Covid-19 and systemic racism, many will recognize that vaccines and anti-racism are unlikely to eradicate these issues that are increasingly and decisively important to key stakeholders. The “new normal” will undoubtedly include the systematic consideration of the risks and opportunities created by the increasing likelihood of pandemics and the legacy of racism in this country. The fact that pandemics dramatically impact vulnerable communities the most will contribute to needed and increasing demands for racial equity. Consequently, the most effective corporate ESG Committees will oversee, direct, drive, and report a systematic engagement with customers, employees, suppliers, host communities, and investors that recognizes Covid-19 and related challenges as the ultimate corporate ESG challenge and opportunity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}