This blog is the second in a multi-part series to help Sustainability and Operating Executives communicate the business case for an ESG Strategy in a way that resonates with the C-Suite.

In a previous blog post ESG Performance Is Now A Mainstream Driver for Shareholder Value, we reviewed some of the persuasive emerging evidence in support of the crystal-clear business case for Corporate Sustainability and C-suite support for strong ESG performance. Even since that blog post, the latest E&Y 2018 Global Climate Change and Sustainability Services investor survey contributed to the tsunami of evidence supporting the importance of ESG management, as it reveals that 97% of investors consider non-financial disclosure in evaluating investment decisions with 89% calling for integrated reporting[1].

With all this evidence in hand, we can conclude that an organized commitment to Corporate Sustainability, manifest in ESG performance, has “crossed the chasm” as a management approach and passed from an Early Adopter Phase to the Early Majority Phase, where disproportionate benefits will accrue most to those on the front end of the phase.[2]

And with this advance the stakes are increasing. Today, the option of not joining the leaders above is posing higher brand risks for senior management:

The above, along with the evidence highlighted in our prior blog ESG Performance Is Now A Mainstream Driver for Shareholder Value, has brought ESG performance front and center for every Board of Directors, CEO and C-Suite managing a public corporation in 2019. Even private companies are paying attention, as the above indicates that their company’s overall true valuation can be influenced by their ESG performance.

The Opportunity: Capturing Disproportionate Benefits for Early Majority

So, here’s the challenge: C-Suite management is increasingly looking for solutions to a problem they do not fully understand. They are busy driving financial performance (as per the above) and are not aware of what can be done today to profitably align their brand with strong ESG performance. Coupled with that, they are sure they do not want to make public (or even private) promises on which they cannot deliver.

Enter the “Management to Leadership” opportunity for middle management Corporate Real Estate (CRE) / Operating executives that we first highlighted in our 2016 CoreNet article “An Unprecedented Opportunity for CRE”. This is exactly where middle management operating executives have a special opportunity to lead on ESG management. While global products companies have to-date deployed sophisticated marketing and supply chain strategies focused on greater global responsibility, the knowledge worker-intensive corporate operations represents an important leadership opportunity for most companies. This is particularly pronounced in service sector companies who do not have responsibility for large manufacturing / supply chain footprint. The space, energy, waste, water and relevant employee engagement long managed by CRE constitutes most of service companies’ environmental impact and makes it possible for CRE and operations to smartly lead on ESG management in a manner that will resonate with the C-Suite. There is an opportunity for middle-managers willing to move beyond an exclusive focus on individual project ROIs, and instead (or additionally) propose the development of a strategy for more “Sustainable Operations” that evolves beyond their traditional (though appropriate) obsession with efficiency. This can be done in a manner that enfranchises additional functions like Human Resources, IT, Procurement and Compliance and better organizes and energizes the conventional commitment to greater efficiency through the added focus incorporating social and environmental performance.

To help middle managers lead on this latent opportunity for the company, catch-up to this megatrend and not miss out on the disproportionate benefits afforded to the Early Majority adopters, we pose some key questions. Operating, CSR, and Sustainability executives can examine these questions to help them build an internal understanding for why Corporate Sustainability has “arrived” as a more strategic approach to management in a world of rising resource constraints, and how their company can profitably follow those corporate leaders in the Early Adopter phase:

In our next blog post, we will affirmatively address the above questions by exploring the key components of best-in-class Corporate Sustainability strategies adopted by the leaders of the Early Adopter phase. These are strategies that the above middle managers can lead in developing and delivering profitably to address the highlighted senior management challenge.

[1] EY. 2018. Does Your Nonfinancial Reporting Tell Your Value Creation Story? November 29, 2018. https://www.ey.com/en_gl/assurance/does-nonfinancial-reporting-tell-value-creation-story

[2] Moore, G. 1991. Crossing the Chasm. HarperCollins.

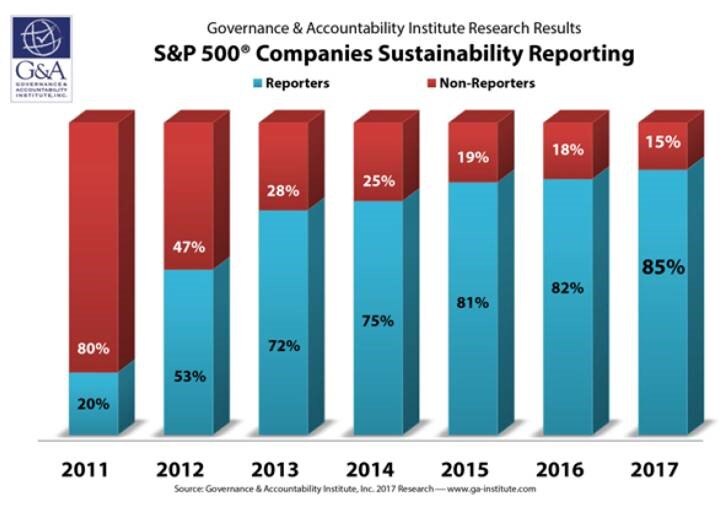

[3] G&A Institute. “85% of S&P 500 Index® Companies Publish Sustainability Reports in 2017.” March 20, 2018.

[4] WWF, Ceres, Calvert, CDP. “Power Forward 3.0: How the Largest US Companies Are Capturing Business Value while Addressing Climate Change. April 2017.

After receiving his MBA, David cut his teeth at Bain & Company in their Boston office and then progressed up to Managing Partner at Booz, Allen & Hamilton (BAH) where he was ultimately elected by his Partners to head their Australasian business. After helping to grow that business from a very early stage to a staff of more than 100, David returned to the US to head BAH’s Retail Financial Services practice in North America. After a few years back in the US market, David transitioned to serve as Managing Partner / EVP at two innovative business service companies: the first a 150 employee, VC-backed innovative technology services provider in Boston, and the second a high-end, 200+ employee proprietary marketing services provider located in Princeton and New York. In both companies, David led over 200% growth within 2-3 years while substantially building the companies’ delivery teams, capabilities and shareholder value

{kind=link}

{kind=link}

{kind=link}