March 19, 2018

By: Roger M. Freeman and James F. Boyle

Executive Summary:

Leading Corporations have determined that the best practice for developing, setting and meeting ambitious renewable energy goals is centered on buying renewable energy from specific, newly-built, large scale wind and solar projects in a breakthrough transaction that can offer both superior environmental claims and superior economics over conventional renewable energy procurement alternatives. Over the past six years, more than 45 leading global corporations have purchased more than 10 gigawatts of renewable energy from new, large scale, renewable energy projects.1 While some were direct purchases, most of these deals utilized a transaction structure regularly referred to as a Virtual Power Purchase Agreement (VPPA). With a VPPA, the renewable energy buyer can acquire Renewable Energy Certificates (RECs) with an unequivocally clear claim that the renewable energy would not exist “but for” the investment of the corporate buyer through the VPPA. These “Bundled RECs”, therefore, have the clear “additionality” top corporations seek as well as a direct and tangible connection to new renewable energy being introduced to the grid and displacing fossil fueled energy (see SR Inc Blog: Not All RECs Are Created Equal). The first generation of these transactions – call it VPPA 1.0 (2013-2017) — were only available to the world’s largest and most sophisticated corporate energy users with the demand and resources to acquire the entire output from a utility scale renewable energy project of 50+ MW and a term of 20 or more years.

In a recent breakthrough, buyer organized aggregated VPPA transactions – VPPA 2.0 — offer the economies of scale and transaction sophistication enjoyed by those world leading corporations to every creditworthy enterprise seeking more credible Bundled RECs. Importantly, VPPA 2.0 also takes advantage of improving market dynamics to allow well represented buyers to negotiate superior deal terms and risk mitigation provisions to create VPPA transactions with both attractive economics and bounded risk. Utilizing these Buy-side Aggregated VPPAs, corporate buyers can develop, set and meet ambitious Renewable Energy Goals through a strategy of committing to acquire load increments of 10MW or less over terms as short as 10 years. In the most attractive deregulated U.S. wholesale markets, VPPA 2.0 provides: (1) more credible “Bundled RECs”; (2) very compelling economics (e.g. conservatively modeled positive cash flows for the buyer in year one and seven figure positive NPVs over a 12 year term); and, (3) robust legal protections in the contract to strictly limit and reduce buyers’ potential financial downside. Even in markets where the fundamental economics are still closing in on the wholesale market price, VPPAs offers energy hedge value. As a result, a well negotiated VPPA 2.0 in the best U.S. markets now provides corporate buyers a potentially profitable path to securing more credible “Bundled RECs” that can be used to offset the greenhouse gas (GHG) emissions caused by their conventional energy use throughout the U.S. (see SR Inc Blog: Renewable Energy For Every Enterprise).

VPPA 2.0 unlocks the corporate and industrial market for renewable energy for the vast majority of high credit enterprises who don’t have the resources or intense energy requirements that were prerequisites of the first generation of VPPA transactions. In addition to enabling new entrants, buy-side Aggregated VPPAs also offer the top corporate buyers from the first generation of VPPAs the opportunity to diversify their portfolio of renewable energy assets through a multi-year, multi-project, multi-market strategy. VPPA 2.0 also enables consortiums of buyers to benefit from expertise of VPPA veterans as they help systemize and scale VPPA 2.0 to help grow the corporate and industrial renewable energy market. For the leading corporate VPPA 1.0 buyers, participating in a VPPA 2.0 transaction could validate the concept and help extend the social and environmental impact of their leadership in this area throughout the economy.

As more high credit enterprises consider how VPPA 2.0 enables them to benefit from the growing cost advantage of newly developed renewable energy projects over existing fossil fueled energy in a growing number of deregulated wholesale electricity markets in the U.S., it is critically important they understand the transaction, as well as its attendant benefits and the related ten risks detailed below that must be managed.

I. Introduction

Corporate Renewable Energy Procurement is taking off. Every week it seems we see another Press Release from a large corporate buyer committing to going 100% renewable or completing the purchase of a new wind or solar farm. Today, more than 120 global corporations have committed to the Climate Group’s RE100 pledge to go 100% renewable. In addition, nearly half of the Fortune 500 have established renewable energy goals and/or carbon emission reduction targets as part of their corporate sustainability strategy.2 Sustainability Roundtable Inc. has worked with more than 75 Fortune 500 companies as multi-year Member-clients over the past decade through a confidential Membership Based Service to assist them in Setting Goals, Driving Progress & Reporting Results internally and externally in their move to more sustainable operations globally. In the last five years the number of Member-clients procuring renewable energy has spiked from less than 20% in 2013 to 100% in 2018. The imperative to achieve a more sustainable corporate energy profile has come from investors, customers, employees and forward thinking management who see clean energy as a strategic corporate opportunity that aligns with the commercial, social and environmental values of company stakeholders. The challenge for corporate officers charged with developing, setting and meeting these goals is to do so in a cost effective manner that benefits shareholders in the near term as well as over time.

Getting to 100% “renewable” or meeting corporate renewable energy goals can be achieved through a variety of strategies, from on-site distributed energy to buying RECs or renewable energy through green tariffs to entering large scale Power Purchase Agreements or PPAs. Starting in the first decade of the 21st Century, companies would most often purchase Renewable Energy Certificates (RECs) to offset their fossil fueled energy use. The RECs would be either qualified for a state Renewable Portfolio Standard or certified by a national certification body such as Green-E. The RECs typically were “unbundled” from the electricity that led to their creation and may have come from a generator that has been in operation for years. More recently, these so-called “unbundled” RECs from existing energy projects have come under criticism due to issues of additionality, accountability and impact. Partially in response to this criticism and due to changing market dynamics improving the economics of utility scale renewable energy, leading corporations have determined that buying unbundled RECs is no longer the best practice for meeting renewable energy goals. Instead, corporations are looking to buy RECs that are tied or “bundled” with the energy from a specific, newly-built renewable energy project and its associated output (Bundled RECS). Bundled RECs are better because the new renewable energy would not exist “but for” the investment by the Corporate buyer. New bundled RECs are truly “additional” and thus have a direct and tangible connection to newly created renewable energy being introduced to the grid and displacing fossil fueled energy. Bundled RECs are now the preferred means for corporate buyers to meet renewable energy goals (see SR Inc Blog: Not All RECs Are Created Equal).

Who’s Buying Bundled RECs?

Over the past six years, global leaders in technology such as Alphabet, Amazon, Apple, Facebook and Microsoft have all purchased the output of large scale wind or solar farms to support their significant power consumption. And it’s not just global tech companies, health care giants Kaiser Permanente and Partners, Dow Jones stalwarts like Dow Chemical and GM, and most recently, leaders in global finance such as Goldman Sachs and JP Morgan – more than 45 world leading firms in all have purchased more than 10 GW of renewable energy through direct and virtual power purchases. These leading corporate buyers have concluded that Bundled RECs are more credible and carry less reputational risk than RECs that are not “bundled” to the purchase of new energy that enables the development of new – more clearly additional – renewable energy. While some of these transactions have involved the direct purchase and delivery of the renewable energy, in most cases, the corporate buyer is using a structured transaction referred to as a Virtual Power Purchase Agreement (VPPA). With a VPPA, the corporate renewable energy buyer can acquire RECs with a nearly unassailable claim that the renewable energy would not exist “but for” the investment of the corporate buyer through the VPPA. The renewable energy produced will have a tangible and direct impact to reduce the carbon emissions and content of the local energy grid.

VPPAs were previously only available to the world’s largest and most sophisticated corporate energy users with the demand and resources to acquire the entire output from a utility scale renewable energy project for a term of 20 years or more. The long term VPPA provided the developer with a bankable revenue stream sufficient to support the financing of the project. A key to the improving economics of these transactions is the buyer’s ability to capture the economies of scale inherent in a large utility scale wind or solar farm of 100MW or more. In a recent breakthrough, the economies of scale and transaction sophistication enjoyed by those world leading corporations are now available through aggregated procurement of bundled RECs to every high credit enterprise seeking more credible RECs in load increments of 10MW or less and terms as low as 10 years.

As more corporate buyers consider buyer organized Aggregated VPPA, or VPPA 2.0, it is critically important that they understand the structure of the transaction as well as the attendant benefits and the related ten risks detailed below.

II. The Virtual Power Purchase Agreement v. Traditional REC purchase

The virtual power purchase agreement structured as a contract for differences (CFD) presents a dramatically different set of rewards and risks than a traditional Unbundled REC purchase agreement. Under a traditional Unbundled REC Purchase Agreement, the buyer agrees to pay a set purchase price for a set quantity of RECs. The seller, often working through a broker or market maker, provides the purchased quantity of RECs. These REC deals are often transferred within an agreed settlement period, and transacted on an annual basis, although one can certainly enter a multi-year agreement. The price of traditional Unbundled RECs can vary greatly – from less than $1 per MWh to more than $300+ per MWh depending on their characteristics including the location of creation, the applicable technology, and most importantly whether they are eligible for use to satisfy state renewable portfolio standard requirements in certain states. The low end of the scale is typically set by wind power RECs from Texas or other south-western states, and the top end applies to solar generated RECs in NJ and Massachusetts. For the most part, corporate buyers have met their objectives buying the cheapest Unbundled RECs available. As noted above, however, questions have been raised about the attribution and additionality of traditional Unbundled RECs. The VPPA was established to provide a mechanism to purchase Bundled RECs, that is renewable energy that is effectively “bundled” together with the energy that created the REC, with the attendant unequivocal attribution and additionality.

III. How A VPPA works — “Buying” renewable energy can actually improve the corporate bottom line

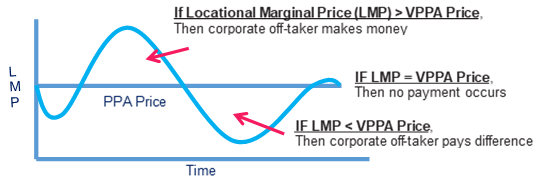

To understand the Risks and Rewards of a VPPA, one must first understand the structure and function of the agreement. Simply put, a VPPA is an agreement to purchase the renewable energy output from a new power plant in the form of Renewable Energy Certificates (RECs) that are clearly and unambiguously attributable to the renewable energy power plant. The Price of these Bundled RECs is established by measuring the difference between the agreed VPPA price and the wholesale market price of energy. As shown in the chart below, under a VPPA, the Corporate buyer received the Bundled RECs created when the RE Facility generates electricity, the Developer/Owner then sells the electricity into the local wholesale market and receives in return the locational marginal price (LMP) at the point of sale.

Looking at the chart, it becomes immediately apparent that the Corporate Buyer can actually make money on the VPPA so long as the LMP is greater than the VPPA price. “Buying” renewable energy through a VPPA can achieve renewable energy goals while actually improving the corporate bottom line. Of course, the Corporate Buyer can lose money too. Moreover, the scope of risk and potential loss is significantly greater than in a traditional Unbundled REC deal. Therefore, in any VPPA transaction, this Price Risk is the most important risk to be quantified, analyzed and mitigated.

IV. Analyzing the Risks and Benefits of a VPPA

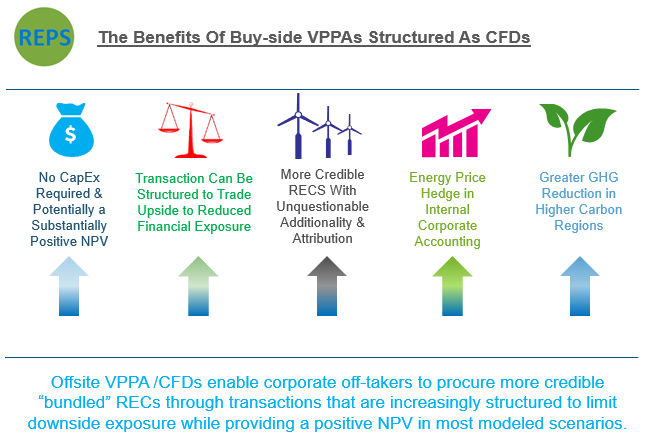

Corporations buying renewable energy or “bundled” RECs through virtual power purchase agreements face a risk/reward calculus that goes well beyond the simple transaction and net cost of buying unbundled renewable energy certificates off-the-shelf. The 3 primary benefits include: (1) a more tangible and credible purchase of renewable energy; (2) the potential for substantial positive net present value; and, (3) long term energy price hedge value. While these benefits offer substantially more value in kind and scope than a conventional REC purchase, there are also risks to be considered. The primary risks include: (1) Market price risks; (2) Operating risks, and (3) Regulatory/accounting risks. These risks and benefits are meaningful and consequential. How they are allocated between buyer and seller can determine the success of your corporate renewable procurement efforts. The remainder of this article focuses on the most important benefits and risks facing the corporate buyer in a VPPA transaction and how they can be managed and mitigated. Two points of context overlaying this discussion is that market dynamics are moving the VPPA transaction terms in favor of the corporate buyer. Moreover, new transaction structures are making the VPPA available to a much broader group of corporate buyers and enabling savvy corporate buyers to better mitigate the risks of the VPPA than in prior iterations.

The Benefits of a VPPA

1.Bundled RECS. A successful VPPA transaction is a true win-win deal for enterprises looking to meet sustainability goals, including renewable energy goals. The bundled RECs acquired through a VPPA are directly attributable to new “additional” renewable energy facility. The new clean energy is being added to the grid and displacing fossil fuels. The project would not happen “but for” the VPPA and it is thus truly “additional” and impactful. As corporate compliance and reporting on energy use and emissions faces increasing scrutiny from stakeholders and the public, procuring bundled RECs has become the best practice solution for meeting corporate renewable energy goals. Simply put, “bundled” RECs (Bundled RECs) are a better product with less reputational risk than “un-bundled” RECs (Unbundled RECs).

2. Positive Net Present Value. If a VPPA opportunity appropriately selected and accurately assessed for market, developer, site, technology, permitting and financing risks as well as carefully negotiated on both business and legal terms, the Bundled RECs acquired can actually have a negative cost, meaning the VPPA will add revenue to the Buyer’s corporate coffers and have positive impact on the corporate bottom line. Unlike a traditional Unbundled REC purchase, which always costs money (however small), the VPPA structured as a Contract for Differences can involve cash flowing in both directions as the Bundled REC “price” is determined by measuring the net difference between the agreed VPPA Price and the wholesale market price of energy. A sustained positive difference between the market price and the VPPA Price will lead to significant positive cash flows for the corporate Bundled REC buyer. This remarkable opportunity begs the question: is this really achievable today or a pipe dream? The reality is that the world is in the midst of an ongoing revolution in energy generation technology and cost. Renewable energy is now the lowest cost source of energy in a growing number of market areas in the US and the world. While Renewable Energy once had to rely on subsidies and incentives to be competitive with the grid, this is no longer true in a number of places. And the trend is accelerating. This new reality is shown in the results from recent utility procurements, as well as the pronouncements of leading market analysts and utility executives. In coming years, renewable energy will be the lowest cost source of energy for large sections of the United States. Right now, there is a great window of opportunity for savvy corporate investors to take advantage of the new market realities while the legacy incentive regimes are being phased out. In the first round of VPPAs, the VPPA price was at or above the market price, and the parties had to rely on forecasts of future energy inflation to determine that the projects would eventually cross over and provide a positive NPV. Now, there are markets where it is possible to secure a long term VPPA where the VPPA Price is substantially below the current market price, meaning that the VPPA will be generating positive cash flow from day one.

3. Energy Hedge Value. One of the first questions confronting a Corporate Renewable Energy Buyer is location – should they seek renewable energy in the markets where they have conventional energy supply? Overlaying this question are the economics of different regions. There is no question that the renewable energy economics, and hence the best VPPA deals, are now in Texas. But what if your load is in PJM or New York, where the VPPA fundamental economics are not as favorable? Some argue that it is important to buy Renewable Energy that will offset the Buyer’s conventional energy supply in that market. Others would say that the ultimate purpose of the transaction is carbon reduction and that is a national market, adding that it is arguably better to offset emissions in a “dirtier,” albeit geographically distant grid. Corporate buyers have taken both paths. Even in markets where the VPPA price is above the current wholesale market price of energy, there is hedge value to entering a VPPA. By entering a long term VPPA, the buyer is locking in the acquisition of Bundled RECs at an agreed value based on the Wholesale Market Price of electricity (WMP). If the WMP rises, then the VPPA buyers’ conventional energy supply costs will also likely rise. The VPPA Buyer will likely make money on the VPPA deal and the profits made thereby can offset higher conventional energy costs. Conversely, if the VPPA price is above the WMP, the Buyer will be paying out cash to the Seller to provide Seller with their required fixed revenue stream, but realizing lower conventional energy costs. In this regard, the VPPA acts as an insurance policy against rising conventional energy costs. However, to properly measure the hedge value, corporate buyers must understand and align their conventional energy supply requirements and the quantity of RECs generated via the VPPA. Moreover, a careful financial analysis is necessary to fully understand the hedging impact and the correlation between the realized value from the VPPA and the conventional price impacts of changing WMP. Corporate buyers must compare the prices they pay and the time of use for conventional energy, with the price of the VPPA transaction. If there is a close correlation, then the hedge will tighter, as movements in the market price affecting the value of the VPPA transaction will have a countervailing impact on the conventional energy costs of the Buyer. Simply put, as market price drops, your conventional energy costs will drop, as will the value of the VPPA transaction. It is important to note that the timing of correlation across markets and time frames can be important. For come corporate buyers, it would be sufficient to see high level of annual correlation as the swings will even out over time.

These three benefits – Bundled RECs, Potential for Positive NPV and Locational Energy Hedge Value make a well structured VPPA transaction a compelling business proposition. This includes selecting a project in a market with high renewable energy potential and consequently low costs, and comparatively higher wholesale market prices. It also includes mitigating the inherent risks in the transaction through contractual terms. The following discussion identifies and highlights 10 of the more salient risks to be considered and mitigated in any VPPA transaction. The issues are complex and can have material consequences.

10 RISKS in A VPPA.

The risks inherent in a VPPA transaction (both VPPA 1.0 and 2.0) can be helpfully placed in three broad categories: Price Risks, Operational Risks, and Legal/Regulatory risks. Across these three categories, ten (10) risks, detailed below, must be managed by a carefully informed internal team and an experienced external procurement team:

I. Market Price Risks: The most important risk to be managed in a VPPA (CFD) is the market price risk. A sustained favorable price differential between the VPPA price and a higher market price can mean literally millions of dollars for the savvy corporate off-taker. Conversely, a bad guess can lead to significant financial loss. These risks include both Forecasting risks and Price Volatility. Below we discuss strategies for mitigating these risks.

1. Forecasting. Prior to entering any VPPA, Corporate buyers should utilize best in class energy price forecasting models and comprehensive financial analysis to analyze, quantify and assess the risk of taking a long position on the price of energy. This analysis can be complex and the forecasting data required to make the best decisions is expensive. For example, VPPAs are typically settled (i.e. the prices are compared) on an hourly basis, so it is important to line up the power production of the renewable energy facility with the appropriate hourly market price. For example, a West Texas wind project typically produces more of its output at night, when the energy prices are typically lower, and less in the afternoon hours of the summer when prices are high. So while the average market price may be higher, the realized market price may be substantially lower. Only the most sophisticated buyers have the resources to perform their own comprehensive financial and market analysis. In most cases, outside dedicated consulting or brokerage expertise can assist Buyer’s with the complexities of financial forecasting and price modeling. With an aggregated procurement, Corporate Buyers can join together to share expertise, analysis and practices as well as the costs of financial forecasting data and analysis.

2. Volatility Risks. Corporate Buyers can also mitigate price risk through the deal terms. Corporate Buyers are now successfully requiring minimum price limits and even price “collars” whereby the Corporate Buyer secures a higher minimum price in exchange for giving up potential profits if the price of energy goes above an agreed ceiling. In both cases, the Buyer will pay a slightly higher VPPA price up front, but the tradeoff is often worth it. In the first rounds of VPPA transactions, the corporate buyer would be expected to cover the difference if the market price of energy dropped below the PPA price, even if the price of energy in the applicable wholesale market dropped below $0. This can happen in very windy markets where there is an oversupply of wind power and operators want to receive the PTC value. This problem has been solved in Buy-Side Aggregated Procurements, where numerous suppliers compete to offer attractive price mitigation structures. It is important to note that by putting a price floor into the deal, the amount of the contract that must be supported on the balance sheet or through a letter of credit is reduced.

3. Scale Risk. The benefit of a positive NPV from day one is in part a function of the large scale of the projects involved. Economies of scale in large renewable energy projects make the economics compelling. However, few corporate buyers have the demand and energy requirements necessary to support investment in a 200 MW Wind farm. However, by joining an Aggregated Procurement with a Buy Side Advised Consortium, Corporate buyers can get the benefit of the large project economies of scale, while only owning a 10MW commitment.

4. Time Risk. The first round of VPPAs were long tenured, reaching out 20-25 years. Longer term PPAs can drive lower borrowing costs, which are then reflected in lower pricing. However, many corporate buyers have much shorter decision horizons and resist entering longer term contracts in any aspect of their operations. The longer term deal will also result in higher potential risk. By reducing the contract term, you can reduce the overall risk of the transaction. This strong preference has been reflected in the competitive process and it is not possible to secure 12 year terms for wind power deals.

II. Operational Risks: Shifted to Seller.

5. Availability. The Contracting Supplier should bear the risk of keeping the plant running on a day to day basis, and the Buyer typically will not share the risk of keeping the facility up and running. VPPAs, like traditional PPAs should include an availability guaranty, to ensure that the Facility will deliver as promised.

6. Congestion and curtailment. The allocation of operational risks also includes the responsibility to bring the power to the market. This can lead to additional Transmission and Distribution (T&D) costs as a result of congestion pricing and/or curtailment if the Facility has interconnected to a line that is overcrowded. While VPPA 1.0 deals varied in their delivery point from the bus bar (at the project) to the regional market hub. Savvy buyers will want the Supplier to bear this risk, and be willing to pay a slight premium in order to settle the contract at the hub.

III. Legal and Regulatory Risks: Shared between Buyer and Seller

7. Change of Law. The energy business is highly regulated. In addition, the market for renewable energy is also highly dependent on a variety of state and federal laws and regulations. When considering a VPPA, the buyers must carefully consider the impact of changes in law. In most cases, a change in law would impact the ability of the Seller to generate and sell the energy as agreed. So a typical change in law provision will give the Seller the ability to terminate the agreement in case of a change in law that has a materially negative impact on the Seller’s ability to perform. Corporate off takers should take care to ensure that any change of law provision is drafted to protect their interests as well, recognizing that the financability of the project may be impacted.

8. Dodd-Frank compliance. As the virtual power purchase agreement involves a financial transaction where the price of the RECs is set in reference to the movements of other prices. As a result, some have argued could be deemed to be a “swap” subject to the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”). Even though as a highly customized, untraded contract, VPPAs are very far beyond the intended reach of Dodd-Frank. Consequently, in an abundance of caution it has become common for VPPA parties to observe the recordkeeping and registration requirements required by Dodd Frank. Typically the Sellers have far more relevant experience and will be willing to serve as the Reporting Party under Dodd-Frank, but corporate buyers should ensure that these requirements are met and responsibility for compliance contractually assigned to the Seller. Moreover, VPPA Off-takers which are financial service firms should recognize that they may have additional obligations when filing in accord with Dodd-Frank.

9. REC certification and compliance. In order to use the RECs to meet renewable energy goals, it is necessary to ensure that the RECs are properly certified by a recognized body in order to maintain their legitimacy. This responsibility should be placed on the Seller, who may set a limit on the costs required to properly certify the RECs.

10. Accounting Treatment. The accounting treatment of a VPPA is important. The typical corporate finance/treasury office will not sign off on any VPPP transaction that would have a balance sheet impact. Nor will they allow any transaction that is required to be treated as a derivative and “marked to market.” While it is important for any corporate buyer to work through the issues with expert advisors, a properly structured VPPA will not be consolidated on the balance sheet of the corporate buyer as it is not a Variable Interest Entity and the VPPA does not constitute a lease. The VPPA should be structured to avoid derivative treatment as well and this can be accomplished by avoiding any “notional amount” of RECs to be acquired. The VPPA should be structured as the right to receive the output from an agreed capacity allocation from the project – also known as an “availability guaranty.” Buyer accounting teams should be into the internal procurement process early to enable them to be educated before the deal is structured and negotiated.

IV. Conclusions

High credit corporate buyers can now see a profitable path in the U.S. to 100% renewable through a Buy-side Aggregated VPPA – or VPPA 2.0 – that provides Bundled RECs from a new, large scale, renewable energy project in the most favorable deregulated wholesale electricity markets in the U.S. And those Bundled RECs can be used to offset the GHG Emissions of the enterprise’s facilities – that are more often than not leased and geographically dispersed – across the U.S. When these Buy-side Aggregated VPPAs are well analyzed, structured, developed and negotiated they can provide more credible Bundled RECs, a substantially positive modeled NPV as well as a hedge against future energy price inflation. These benefits are substantial and are far superior to the costs of the traditional unbundled REC purchase. A typical publicly traded fast growth technology firm with a total annual electricity demand for its own facilities that could be met by 10 to 30 MW of Wind or Solar capacity, might achieve its initial Scope 1 and 2 one hundred percent renewable energy goal through just two years of planning and two to three smaller (e.g. 10 MW with 12 years of term) VPPA 2.0 transactions, each conservatively modelled to be in the money year one for the buyer and providing a seven figure NPV over term. There are, however, risks inherent in any VPPA that must be identified and managed. These risks include market prices, operational risks and legal/regulatory risks. These risks can be addressed and mitigated through a carefully informed internal team with the assistance of Buy-side Advisors with deep relevant expertise in renewable energy markets, financing, law, technology, corporate procurement and deal structuring; who can provide strategy development as well as financial analysis and a structuring of the transaction through business and legal negotiations that favor the buyers. Currently, a historically low but changing interest rate environment and substantial but declining federal tax subsidies has helped create intense competition among top developers that is providing a pronounced “buyers’ market” for high credit corporate buyers. In select deregulated wholesale markets in the U.S., the price of developing and delivering new renewable energy is currently substantially below the historically low and currently prevailing local marginal price. Consequently, high credit buyers procuring through a Buy-side Aggregated VPPA can reasonably hope to lock in deals in these most favorable markets that are conservatively modeled to be “in the money” in year one. Moreover, through competitively sourced Buy-side Aggregated VPPAs, consortiums of corporate off-takers are winning better deal terms including: lower prices, shorter terms, and robust legal protections against downside financial exposure. Taken together, these changes constitute the emergence of VPPA 2.0, which is a breakthrough that is changing the fundamental question regarding corporate procurement of renewable energy from “how much will it cost?” to “how much, conservatively, will it make?”

1. Business Renewable Center, Deal Tracker, 2018 (SR Inc has supported the Rocky Mountain Institute’s Business Renewable Center since its inception in 2015 and is a proud current sponsor)

2. The Climate Group, RE 100, 2018

Select Relevant SBER Executive Guidance & Tools:

- Member Advisories:

- Member Briefings

- Solar Power Purchase Agreements (SPPAs)

- International Markets for Renewable Energy Certificates (RECs)

- Managing the Changing Water-Energy Nexus

- Impact of Renewable Energy Purchases on Reporting

- International Renewable Energy Markets: 2016 Update

- Market Structure for Conventional and Renewable Energy

- Presentations:

- Summit for Sustainable Operations VI: Renewable Energy Portfolio-wide – Envisioning Breakthrough

- 2017 Q3 Symposium: Powering Portfolio-wide Real Estate & Operations with Renewable Energy

- 2017 Q2 Symposium: Renewable Energy Portfolio-wide

- 2017 Q1 Symposium: Renewable Energy Portfolio-wide

- Summit for Sustainable Operations V: Regenerative Portfolios by 2030

Roger Freeman is the Managing Director of Sustainability Roundtable Inc.’s Renewable Energy Procurement Service (REPS), a dedicated consulting service providing Buy-side Only Advisory for on-site and off-site corporate renewable energy procurement. Roger has led at the intersection of alternative energy development, procurement, law and regulation for more than twenty years. He has personally led in developing hundreds of MW of wind and solar throughout the United States and has served as the lawyer, financier and advisor to institutional and Fortune 500 clients on renewable energy globally. As Managing Director of Energy Ventures for Citizens Energy, he managed renewable energy and energy efficiency businesses. As the founder of a solar development firm he personally led in developed more than a dozen solar energy projects. He is a graduate of Oberlin College and the University of Virginia School of Law. Roger served on the Board of Advisors of Distributed Energy Magazine and is an elected member of the Power & Light Board in Hingham, MA.

Jim Boyle is CEO & Founder of Sustainability Roundtable, Inc. For nearly ten years, Jim has led full-time teams of diverse experts assisting world-leading corporations, real estate owners, and federal agencies in their move to greater sustainability. He has led in developing SR Inc’s confidential, industry specific, annual management assessment and recommendation process for more sustainable operations and real estate that is compatible with major public standards globally. Further, he has directed the development of hundreds of pieces of SR Inc original, case based Management Best Practices Research and Executive Guidance & Tools available in SR Inc.’s digital library. Mr. Boyle also led in the creation of SR Inc’s Renewable Energy Procurement Services (REPS), which advises and represent Fortune 500 Member-clients and rapidly growing public companies across the U.S. and internationally in the development of Renewable Energy Strategies and the procurement of both on and off-site advanced energy solutions. Before founding SR Inc, Mr. Boyle advised fast growth technology firms, private equity firms, and institutional investors as an adviser on real estate strategy and transactions, and before that, as a large law firm attorney assisting corporate and investment clients on complex real estate and environmental compliance-related issues. He co-led Trammell Crow Company Corporate Advisory Services in San Francisco and returned to his native Boston and Trammell Crow Company’s market leading team in Greater Boston where he received the Commercial Brokers Association’s Platinum Award for the highest level of commercial real estate transactions. While at Trammell Crow Company, he incorporated and was the principal co-founder of the Alliance for Business Leadership, a MA based non-profit for CEO, investors and business leaders who share a commitment to public policy that advances a more broadly shared and sustainable prosperity. Jim is a graduate of Middlebury College and Boston College Law School, who early in his career served as a federal law clerk, an aide to John F. Kerry in the U. S. Senate and on Vice President Al Gore’s campaign for President. He lives in Concord, MA with his wife and two children and writes and speaks regularly on management best practices in more sustainable business. See e.g., Could LEED for Existing Buildings Transform the Building Industry, Urban Land and An Unprecedented Opportunity & Moment for CRE, CoreNet Global, LEADER, September 2016.