Driven by knowledgeable corporate buyers, economics that can beat natural gas (and which are improved by brutal developer competition), as well as by an expectation of both increased interest rates and decreased federal tax credits, utility scale Wind in the U.S. is being lifted by a perfect storm of drivers to record highs of new deals closed in Q4 2018.

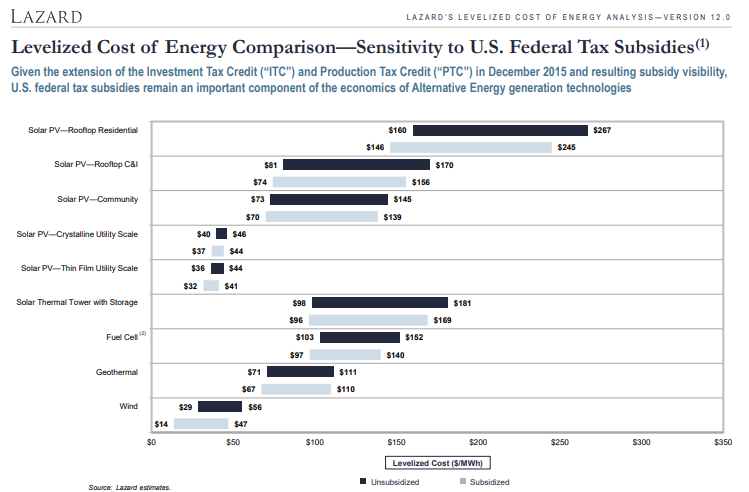

Lazard Levelized Cost of Energy Analysis – Version 12

According to Bloomberg New Energy Finance on June 30th, 2018, the installed capacity of Wind and Solar technologies globally had exceeded 1000 Giga Watts (i.e. a Terra Watt). That reflects a 65 fold increase since 2000 and a quadrupling of installed capacity since 2010. Of that total, 54% was Wind and Solar (especially utility scale Solar) was growing even more quickly than Wind to become 46% of that total TW of installed Wind and Solar capacity. One of the drivers of utility scale Wind in the U.S. has been the corporate and industrial segment of buyers in deregulated wholesale electricity markets in the U.S. who have discovered that at utility scale Wind (and sometimes even Solar) produces electricity less expensively than coal and natural gas fired plants in a growing number of U.S. markets.

Global information, communication and technology (ICT) firms like Alphabet, Apple, Amazon and AT&T, in particular, have led in seeking to participate in the cost advantage of large scale Wind and Solar as they use these nearly zero marginal cost capital projects to hedge the volatility of the cost of the enormous electricity demands of their data centers. More recently, more regular sized corporations without the “super intense” localized demand of a data center have sought out utility scale wind and solar projects to make possible – and drive towards – ambitious environmental goals. These companies serve as “Corporate Off-takers” in Virtual Power Purchase Agreements (VPPAs) structured as Contracts for Differences (CFDs) wherein they make a long-term commitment to a minimum VPPA Price the developer will receive which enables the developer to get the new development financed. And the fact that average VPPA Prices Corporate Off-takers can now lock-in are regularly below historically low, current, market prices has made Corporate VPPA/CFDs very popular.

Business Renewables Center, Deal Tracker

Corporate Off-takers now regularly commit for 12 or more years for Wind and 15 or more years for Solar. Corporate Off-takers without “super intense” localized data center or manufacturing related demand, enter into these VPPA/CFDs primarily to procure the national Renewable Energy Certificates (RECs) associated with each mega watt hour of electricity produced by the new renewable energy plant. These Corporate Off-takers then apply those “Bundled RECs” (i.e. RECs bundled into the same contract that finances the new renewable energy plant) against the Green House Gas (GHG) emissions associated with the electricity they buy through-out the U.S. (including electricity they buy in regulated markets since these “Virtual” PPAs are financial transactions that do not impact their existing procurement and use of electricity). Corporate Off-takers may also use the VPPA Price performance against the Local Marginal Price the developer is able to realize as a hedge in their internal accounting of their utility costs for the grid electricity they continue to procure to supply their facilities. Since when their conventional grid prices go up, they will regularly be making money on their VPPA/CFDs as the developer pays the Corporate Off-taker the margin above the minimum VPPA price the Corporate Off-taker has committed to pay the developer.

Once the province of only the world’s largest energy users with extensive energy teams, VPPA/CFDs have become the preferred way for high-credit corporates to procure RECs. Universities including Boston University (which recently announced a VPPA enabling it 100% renewables commitment) and MIT (a long-time SR Inc Member-client) as well as hospitality leaders like Vail Resorts have committed to VPPA/CFDs to obtain RECs and advance ambitious GHG emission reduction goals. Primarily because “Bundled RECs” from VPPA/CFD projects are more credible than “Unbundled RECs” that are not necessarily tied to additional renewable energy, even if they have the respected Greeen-E certification.

Second generation of Corporate Off-takers regularly have the relatively low intensity, geographically dispersed, electricity demand of the information and service companies (which increasingly outsource their servers) that dominate job growth in the U.S.. These firms generally frown on long-term transactions but they recognize that their most sought after talent, customers and investors do want them to do their part in supporting the development of additional renewable energy and reducing GHG emissions. Which is why these firms want the Bundled RECs to prove they are supporting the creation of the renewable energy and off-setting their continued purchase of conventionally produced electricity. Through this process, Bundled RECs have become the heart of many leading corporations’ sustainability programs and often the “secret sauce” that enables them to publish and pursue ambitious strategies to cut in half or even zero our their net GHG emissions. Since generally they can reduce less than 30% of their GHG emissions through efficiency gains or financially viable on-site renewable energy.

These second generation Corporate Off-takers are regularly the growth firms of a service economy and in-part because of the battle for talent as they grow, they are people focused. They can only access the transaction sophistication and economies of price afforded by VPPA/CFDs if they join with one of the huge first generation of Corporate Off-takers as SR Inc Charter Member Akamai Technologies did in partnering with Apple Inc. for a small part of a transaction Apple dominated; or through engaging in a Aggregated Procurement with organizations similar to them as multiple SR Inc Charter Members are doing separately and, in multiple instances, together with other SR Inc Member-clients. And most all aggregation efforts underway are intent in signing large scale Wind deals before the end of 2018.

Sustainability Roundtable, Inc. Renewable Energy Procurement Services (REPS)

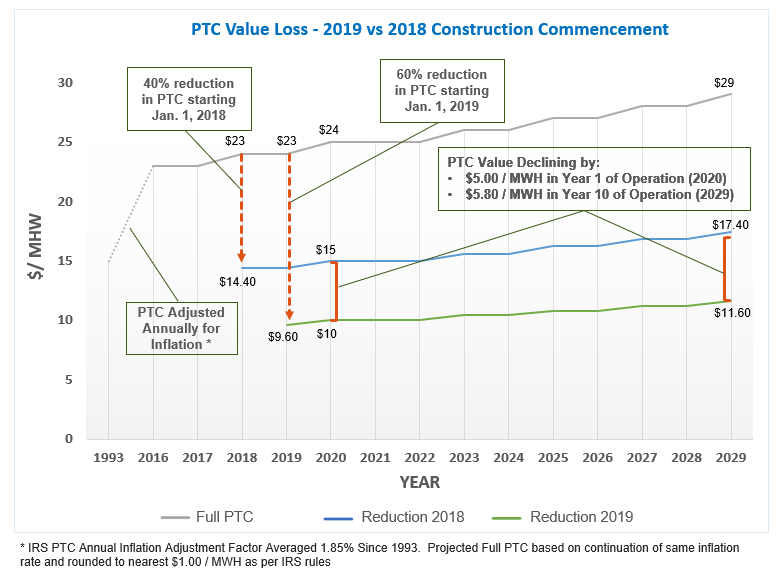

In fact, by the time the non-profit Business Renewables Center’s (which SR Inc has been proud to Co-sponsor) convened its Renewable Energy Buyers Alliance Summit in October this year, 2018 had already exceeded any other year with Corporate Off-takers signing for more than 5 GW of new, large scale, Wind and Solar projects in deregulated wholesale markets in the U.S. Moreover, since average VPPA Prices for wind projects in several markets has dropped substantially below current market prices due, in part, to the hefty federal Production Tax Credit (PTC) for Wind that will decline a further 40% January 1st, 2019 and because interest rates are expected to continue to rise – the number of wind deals closing in just Q4 2018 is also expected to be without historical precedent.

It seems clear that the number and scope of VPPA/CFDs signed by Corporate Off-takers has spiked to historic highs in 2018 and will spike further in Q4 of 2018. Moreover, the substantial January 1st, 2019 reduction in the Production Tax Credit (PTC) in the U.S. will make new large scale wind projects more expensive to build, if they are not “grandfathered” to benefit from the larger PTC value through the PTC’s liberal definition of what it is to ‘Commence Construction in 2018″ which is required for the full PTC value.

Bloomberg New Energy Finance

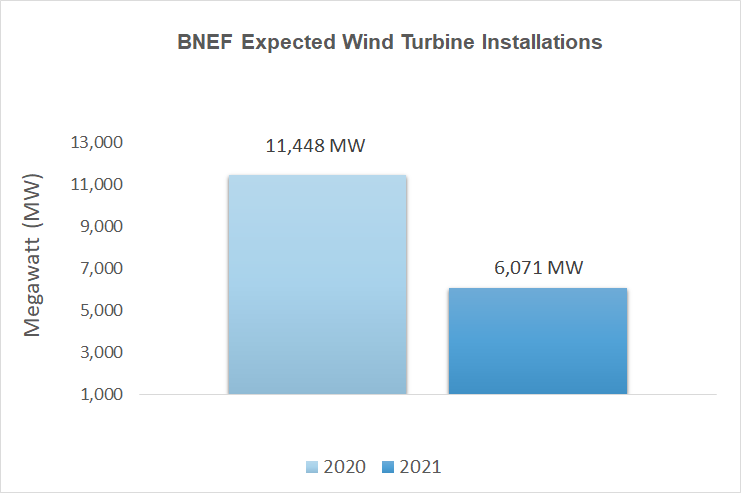

The stepped reduction of the PTC in 2019 combined with rising interest rates is expected to substantial reduce the number of deals closed in 2019 and 2020 and drive a dramatic drop-off of installations from a record 11.4 GW in 2020 to 6 GWs in 2021. Meanwhile, utility scale Solar is still trending up in popularity with Corporate Off-takers as the far richer VPPA Prices of utility scale Solar begins to decline more towards large scale Wind’s average VPPA Prices and the Investment Tax Credit (ITC) used in large scale Solar projects declines more slowly than the PTC, making it possible large scale Solar best days may be ahead of it. But for large scale Wind, Q4 2018 appears to provide a perfect storm of drivers lifting scaled Wind in the U.S. to historically low prices and installation rates that are unlikely to be seen again for years.

Jim Boyle is CEO & Founder of Sustainability Roundtable, Inc. For more than ten years, Jim has led full-time teams of diverse experts to assist nearly 100 Fortune 1000 companies on a multi-year basis in their move to more sustainable high-performance. Specifically, SR Inc has helped world-leading corporations, real estate owners and federal agencies to Set Goals, Drive Progress & Report Results in greater Corporate Sustainability. Jim has led in developing SR Inc’s confidential, industry specific, annual Management Assessment and Recommendation process for more sustainable global operations and energy that is compatible with major standards. Further, he has directed the development of hundreds of pieces of SR Inc original, case based Management Best Practices Research and Executive Guidance & Tools available in SR Inc.’s digital library. Mr. Boyle led in the creation of SR Inc’s Renewable Energy Procurement Services (REPS), which advises and represent Fortune 1000 Member-clients and fast growth technology companies across the U.S. and internationally in the development of Renewable Energy Strategies and the procurement of both on and off-site advanced energy solutions. Before founding SR Inc, Mr. Boyle advised fast growth technology firms, institutional investors and private equity firms as an adviser on real estate strategy and transactions, and before that, as a large law firm attorney assisting corporate and investment clients on complex real estate and environmental compliance-related issues. He co-led Trammell Crow Company Corporate Advisory Services in San Francisco and returned to his native Boston and Trammell Crow Company’s market leading team in Greater Boston where he received the Commercial Brokers Association’s Platinum Award for the highest level of commercial real estate transactions. While at Trammell Crow Company, he incorporated and was the principal co-founder of the Alliance for Business Leadership, a MA based non-profit for CEO, investors and business leaders who share a commitment to socially responsible business practices and public policy. Jim is a graduate of Middlebury College where he co-captained the football team and Boston College Law School, who early in his career served as a federal law clerk, an aide to John F. Kerry in the U. S. Senate and on Vice President Al Gore’s campaign for President. He lives in Concord, MA with his wife and two children and writes and speaks regularly on best practices in more sustainable business. See e.g., Could LEED for Existing Buildings Transform the Building Industry, Urban Land and An Unprecedented Opportunity & Moment for CRE, CoreNet Global, LEADER.

Stay on top of the latest SR Inc insights

Every quarter, learn about new corporate ESG best practices, case studies, executive event takeaways, best practice guidance and tools on various subjects, SR Inc team updates, and more!

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.