October 23, 2018

SR Inc REPS Presents on Three Enabling Breakthroughs

More than four hundred leading, invited, corporate buyers, developers and service providers in large-scale renewable energy gathered in Oakland last week for the 3rd annual Renewable Energy Buyers Alliance (“REBA”) Summit, where Aggregated Procurement of large-scale renewables took center stage.

I was pleased to join Sustainability Roundtable Inc.’s Renewable Energy Procurement Services (“REPS”) Managing Director, Roger Freeman, to lead multiple packed discussions in the main room at the Oakland Convention Center regarding enabling contractual breakthroughs in the Buy-side Aggregated Virtual Power Purchase Agreements (“VPPAs”). It was outstanding to observe that Buy-side Aggregated VPPAs – what SR Inc REPS team has recognized as “VPPA 2.0” – had clearly become the central topic of REBA’s 2018 Summit with nearly a dozen related interactive sessions filled to capacity.

Amid reports from the Rocky Mountain Institute’s Business Renewable Center that year-to-date, corporate buyers have signed for a record-breaking 5 GWs of off-site, utility-scale, renewable energy in the U.S., Roger Freeman and I were delighted to share three breakthroughs that had benefited multiple SR Inc Member-clients. These are breakthroughs many SR Inc Member-clients have sought for years but it was only in 2018 that: (a) the improved and remarkable economics of new utility-scale renewable energy (which is now a lower cost generator than coal or natural gas in multiple U.S. markets [1]); (b) fierce top developer competition; and, (c) the time sensitivity of declining federal tax credits and rising interest rates – prompted these buyer favorable terms to be provided and financed by the most competitive developers in 2018.

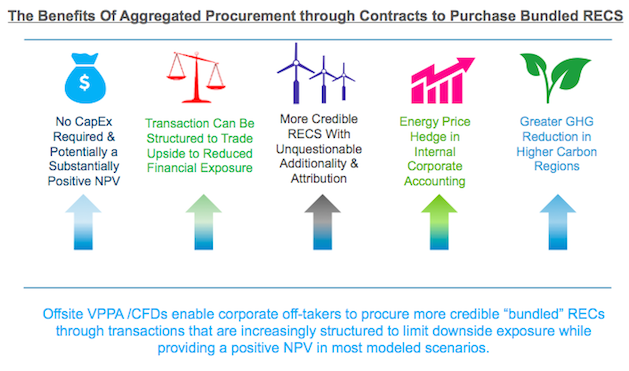

Each of these innovations help confirm that Buy-side Aggregated VPPAs represent an enduring evolution of the VPPA transaction that remains structured as a Contract for Difference (i.e. with the net, positive or negative, of the VPPA Price against the Locational Marginal Price flowing to the Corporate Off-taker). Now multiple corporate buyers can substantially de-risk the procurement of more credible Bundled Renewable Energy Certificates (i.e. “RECs” that are unquestionably tied to new renewable energy because they are bundled into the same Power Purchase Agreement that finances the new project – see Not All RECs Are Created Equal) by joining together through Buy-side Aggregated VPPAs to take far smaller, customized, amounts of capacity (e.g. 10 MW), while still winning the remarkable economics of price associated with 100+ MW of utility-scale renewable energy. And also benefiting from the specialized expertise of top service providers as well as the transaction sophistication of no cap ex VPPAs which, previously, were only available to the world’s largest companies like SR Inc’s earliest and largest Charter Members.

Consequently, Buy-side Aggregated VPPAs – or VPPA 2.0 – significantly democratizes the cost advantage of utility-scale renewable energy. And the cost advantage enjoyed by utility-scale renewables is substantial in a growing number of deregulated wholesale electricity markets in the U.S. where average VPPA Prices (the minimum price to which Off-takers commit to help finance the project) are 30+% below the current average grid price and even 20+% below the current wind and solar production adjusted prices. Until SR Inc Charter Member MIT pioneered Buy-side Aggregated VPPAs in 2016 with the Boston Medical Center (i.e. the hospital of last resort in Boston) and the Boston Non-profit, A Better City, there had only been one or two public sector and university Aggregated VPPAs in the U.S. As a result, most all of the 14+ GWs of utility-scale Wind and Solar financed by corporate VPPAs (i.e. Contracts for Bundled RECs) since 2012 have been signed by single off-takers.

Now with the traditional 25 year off-site PPA term cut in half to a regular 12 years for Wind and 15 years for Solar, and with Aggregated Procurements enabling the Off-take of far smaller amounts of capacity, the more than 99% of even large enterprises that do not have the sufficient “super intense” localized energy demand to drive the creation of a utility-scale renewable energy project, can now benefit from the clear financial and environmental advantages of new utility-scale renewable energy in the U.S.

What SR Inc REPS discussed with top corporate buyers last week in Oakland was by no means the market norms. It was instead the newest Corporate Off-taker favorable terms SR Inc Members-clients – and others – have been able to win in multiple U.S. markets in the second half of 2018. Although the REPS Senior Team (20+ year experts in renewable energy development and related contracting, regulations, financing and technology) has advocated for and observed more than a dozen important improvements in Member-client VPPAs over the last six years, we highlighted three changes high credit Off-takers (e.g. BBB- or better) can win when participating in Aggregated Procurements through working constructively with most experienced and regularly best financed developers for a mutually winning partnership in new renewable energy.

1. Exclusive Contractual Privity:

Specifically, we discussed how the most confident, large scale, wind and solar developers were willing to offer the multiple Off-takers presented in the aggregation: Exclusive Contractual Privity. This means that trusted and established aggregators can prompt top developers to provide each individual Off-taker in an aggregation with nearly identical, non-binding, Letter of Intents (LOI) that are not in any way dependent on the other LOIs in the aggregation and which promise a VPPA with the developer that is also in no way dependent on the other VPPAs in the proposed Aggregation. This requires, of course, that the developer is assured the aggregator represents sufficient individual Off-takers and combined demand to warrant the price and terms agreed in the equally independent – but nearly identical – LOIs. Significantly, this reliance on independent but nearly identical non-binding LOIs free the Off-takers from the need to enter into sometimes complex joint venture agreements with other Off-takers before the Aggregation; which multiple experienced Off-takers have complained can take months to negotiate and may not result in an actual Aggregated VPPA of the sought Bundled RECs.

2. Financial Collars

Back in 2012-2013 when SR Inc Charter Members began pioneering Power Purchase Agreements structured as Contracts for Difference, specialized counsel regularly referred to these transactions as “Contracts to Purchase Variably Price RECs”. Some have lamented the loss of that name [2] – which was more legally descriptive and threw into high relief the need to get the contract to purchase right, since that was what concerned the Off-taker, more than the successful financing, development and operation of the project, which is the responsibility of the developer. Indeed, the prevalence of the terms “VPPA” and Contracts for Difference (CfD) suggest that developers and not Corporate Off-takers have dominated this market that is still only six years old. There is particular benefit to describing VPPAs as Contract to Purchase Bundled RECs (SR Inc REPS’s preferred term) now that a new generation of buyers has begun to shape the market and they are more interested in the procuring of more credible Bundled RECs than energy hedges.

Since at least 2013, Buy-side Advisors have been attempting to introduce a bounding of the variability of the price of the REC in the settlement between the Developer and the Off-taker. And for all that time Developers and, more specifically, their financial partners have resisted these attempts as undercutting the value of the credit the Off-taker provides. But one important development has occurred to help bring Financial Collars to the market for Contracts to Purchase Bundled RECs – if still rarely – in 2018.

This new development is the type of Corporate Off-taker that is shaping the market. Several top developers have begun to realize that the far larger, second, generation of Corporate Off-takers has inverted the priorities of the first generation of Corporate Off-takers. First generation Off-takers sought grid proximate energy hedges and more credible Bundled RECs – in that order. The second generation of Corporate Off-takers has far smaller individual needs but represent a far larger market, and they prioritize the procurement of more credible Bundled RECs. In fact, second generation buyers are corporate procurement offices, not energy teams at top energy users. Consequently, procurement procedure and authority has shaped the maximum theoretical possible loss. Reducing that number – however remote of possibility it represents – helps all parties.

Consequently, global developers investing in market share and self-financing national developers have reached to offer one form of a financial collar or another. In each instance, the developer seeks to limit Off-taker’s financial downside exposure in exchange for the developer securing a higher VPPA Price and/or more of the financial upside above the VPPA Price. And although transactions structured to rely on third-party financial firms to provide collars have experienced difficulties (e.g. the prospect of triggering derivative accounting for the Off-taker), in the second half of 2018, top developers are willing to post security against them failing to secure the financing of the collared structure they propose, even if only a precious few have already succeeded with third-party financing in U.S. markets.

3. Upside Share Structures

In what is still a nascent and highly dynamic Contract for Bundled RECs market, SR Inc REPS has been pleased to see multiple top developers in multiple U.S. markets provide transaction structures designed to align incentives between the Developer and Corporate Off-taker. Some developers have done this in a manner that appreciates the Second Generation of Corporate Off-taker that is especially risk adverse and without real ability to capture internal recognition or award for upside financial performance. They have offered pricing structures that provide real time – as opposed to annually adjusted – zero minimum settlements (to avoid the bad optics of the Off-taker’s often HQ located relevant office writing checks for remote below zero dollar wind energy), in return for a sharing of upside above the VPPA Price. SR Inc REPS has seen anywhere from 75% to 10% of the realized price above the VPPA Price flowing to the Developer. Interestingly, a meaningful upside split to the developer can lessen the pressure to stipulate in the Contract to Purchase Bundled RECs all a best-in-class developer and operator must do to consistently drive realized sale price above the VPPA Price. As it provides an incentive for the developer to continue to invest (e.g. in the expected addition of storage) in the project to realize margin above the VPPA Price. While – most importantly – it also enables the Developer to lower the VPPA price.

Conclusion:

Buy-side Aggregated VPPAs – VPPA 2.0 – make it possible for an exponentially larger market of high-credit enterprises to participate in the financial and environmental advantages of large-scale renewable energy. Top developers are now willing to compete to provide impressively organized and aggregated Off-takers with individual LOIs and VPPAs that are not dependent on the other participants’ LOIs and VPPAs. More than a dozen plus top developers are even willing to provide a transaction structure to reduce downside financial exposure, and an elite few will even provide an upside share structure to align incentives and lower the VPPA Price.

This all points to the fact that the 14+ GW market for large-scale, Off-site, renewable energy in the U.S. (and beyond) is ready to blossom. As it becomes the market for Contracts to Purchase Bundled RECs. What many began to see out in Oakland last week was that Buy-side Aggregated VPPAs could provide more credible Bundled RECs to every high-credit enterprise. (For an in-depth explanation, see: Renewable Energy For Every Enterprise). Enabling it all, is a new type of contract – the VPPA 2.0 – that is tailored for a new generation of Corporate Off-takers. Before relevant federal tax credits decline and interest rates increase, the year one Cash Flows and NPVs that our Member-clients are regularly modeling will shock many. Especially those who have not yet internalized: new utility-scale renewable energy increasingly provides the lowest cost of generation even before substantial but declining subsidies – which scores of leading Corporate Off-takers and developers are pursuing – as 2018 shatters all large scale, Off-site, PPA records.

[1] Lazard’s Levelized Cost of Energy Analysis, Verizon 11.0

[2] What Change Requires: Off-Site Power Purchase Agreements

Select Relevant SBER Executive Guidance & Tools:

- Member Advisories:

- Member Briefings

- Solar Power Purchase Agreements (SPPAs)

- International Markets for Renewable Energy Certificates (RECs)

- Managing the Changing Water-Energy Nexus

- Impact of Renewable Energy Purchases on Reporting

- International Renewable Energy Markets: 2016 Update

- Market Structure for Conventional and Renewable Energy

- Presentations:

Jim Boyle is CEO & Founder of Sustainability Roundtable, Inc. For more than ten years, Jim has led full-time teams of diverse experts to assist nearly 100 Fortune 1000 companies on a multi-year basis in their move to more sustainable high-performance. Specifically, SR Inc has helped world-leading corporations, real estate owners and federal agencies to Set Goals, Drive Progress & Report Results in greater Corporate Sustainability. Jim has led in developing SR Inc’s confidential, industry specific, annual Management Assessment and Recommendation process for more sustainable global operations and energy that is compatible with major standards. Further, he has directed the development of hundreds of pieces of SR Inc original, case based Management Best Practices Research and Executive Guidance & Tools available in SR Inc.’s digital library. Mr. Boyle led in the creation of SR Inc’s Renewable Energy Procurement Services (REPS), which advises and represent Fortune 1000 Member-clients and fast growth technology companies across the U.S. and internationally in the development of Renewable Energy Strategies and the procurement of both on and off-site advanced energy solutions. Before founding SR Inc, Mr. Boyle advised fast growth technology firms, institutional investors and private equity firms as an adviser on real estate strategy and transactions, and before that, as a large law firm attorney assisting corporate and investment clients on complex real estate and environmental compliance-related issues. He co-led Trammell Crow Company Corporate Advisory Services in San Francisco and returned to his native Boston and Trammell Crow Company’s market leading team in Greater Boston where he received the Commercial Brokers Association’s Platinum Award for the highest level of commercial real estate transactions. While at Trammell Crow Company, he incorporated and was the principal co-founder of the Alliance for Business Leadership, a MA based non-profit for CEO, investors and business leaders who share a commitment to socially responsible business practices and public policy. Jim is a graduate of Middlebury College where he co-captained the football team and Boston College Law School, who early in his career served as a federal law clerk, an aide to John F. Kerry in the U. S. Senate and on Vice President Al Gore’s campaign for President. He lives in Concord, MA with his wife and two children and writes and speaks regularly on best practices in more sustainable business. See e.g., Could LEED for Existing Buildings Transform the Building Industry, Urban Land and An Unprecedented Opportunity & Moment for CRE, CoreNet Global, LEADER.

Jim Boyle is CEO & Founder of Sustainability Roundtable, Inc. For more than ten years, Jim has led full-time teams of diverse experts to assist nearly 100 Fortune 1000 companies on a multi-year basis in their move to more sustainable high-performance. Specifically, SR Inc has helped world-leading corporations, real estate owners and federal agencies to Set Goals, Drive Progress & Report Results in greater Corporate Sustainability. Jim has led in developing SR Inc’s confidential, industry specific, annual Management Assessment and Recommendation process for more sustainable global operations and energy that is compatible with major standards. Further, he has directed the development of hundreds of pieces of SR Inc original, case based Management Best Practices Research and Executive Guidance & Tools available in SR Inc.’s digital library. Mr. Boyle led in the creation of SR Inc’s Renewable Energy Procurement Services (REPS), which advises and represent Fortune 1000 Member-clients and fast growth technology companies across the U.S. and internationally in the development of Renewable Energy Strategies and the procurement of both on and off-site advanced energy solutions. Before founding SR Inc, Mr. Boyle advised fast growth technology firms, institutional investors and private equity firms as an adviser on real estate strategy and transactions, and before that, as a large law firm attorney assisting corporate and investment clients on complex real estate and environmental compliance-related issues. He co-led Trammell Crow Company Corporate Advisory Services in San Francisco and returned to his native Boston and Trammell Crow Company’s market leading team in Greater Boston where he received the Commercial Brokers Association’s Platinum Award for the highest level of commercial real estate transactions. While at Trammell Crow Company, he incorporated and was the principal co-founder of the Alliance for Business Leadership, a MA based non-profit for CEO, investors and business leaders who share a commitment to socially responsible business practices and public policy. Jim is a graduate of Middlebury College where he co-captained the football team and Boston College Law School, who early in his career served as a federal law clerk, an aide to John F. Kerry in the U. S. Senate and on Vice President Al Gore’s campaign for President. He lives in Concord, MA with his wife and two children and writes and speaks regularly on best practices in more sustainable business. See e.g., Could LEED for Existing Buildings Transform the Building Industry, Urban Land and An Unprecedented Opportunity & Moment for CRE, CoreNet Global, LEADER.